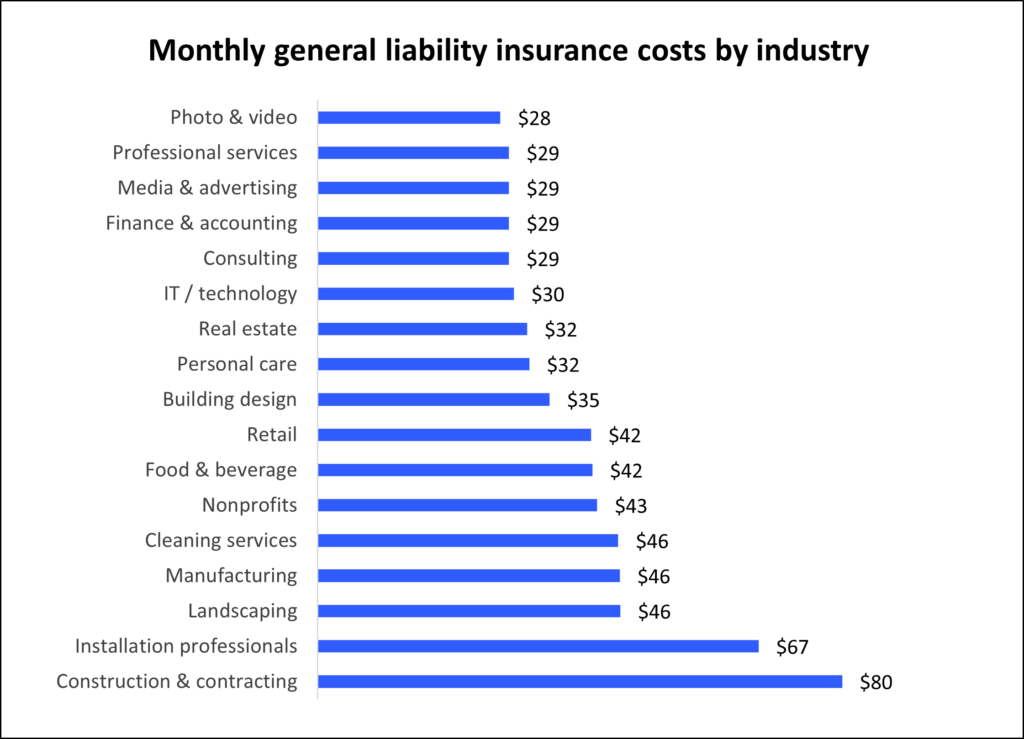

IT consultants

Carpenters

General contractors

Computer repair and installation

Restaurants

Engineers

Janitorial services

SaaS companies

Management consultants

Telecom companies

Data centers

Accountants and CPAs

House cleaning

Fast food restaurants

Advertising agencies and consultants

Lawn care

Electricians

Painters

Web developers

Lawyers

Doctors

Marketing consultants

Clothing stores

Landscape design

Flooring installation

IT consultants

Carpenters

General contractors

Computer repair and installation

Restaurants

Engineers

Janitorial services

SaaS companies

Management consultants

Telecom companies

Data centers

Accountants and CPAs

House cleaning

Fast food restaurants

Advertising agencies and consultants

Lawn care

Electricians

Painters

Web developers

Lawyers

Doctors

Marketing consultants

Clothing stores

Landscape design

Flooring installation