Choose from the nation's best insurance providers

Commercial Property Insurance

Commercial Property Insurance

Commercial property insurance pays to repair or replace stolen, lost, or damaged business property. It covers your business’s physical location and other assets like equipment.

Why is commercial property insurance important for small businesses?

Commercial property insurance protects against the risks of owning or renting an office, storefront, or other business property. It covers property losses when a fire damages your office, or a pipe bursts and floods your store.

Items that are covered include:

- Inventory

- Furniture and fixtures

- Computers and electronics

- Tools and equipment

- Broken windows and structural damage

- Lost income (when your policy includes business interruption insurance)

If you rent a commercial space, your landlord may require you to carry this coverage. Even when it’s not required, commercial property insurance is important for any small business that owns physical assets.

You may also see this type of insurance referred to as business hazard insurance.

Businesses that purchase a policy typically:

- Own or rent a building, store, or office

- Own or rent expensive equipment or tools

- Have products or inventory

- Depend on other valuable business assets

What does commercial property insurance cover?

Commercial property insurance covers your business’s real estate and its contents. It helps pay for repair or replacement when business property is lost, damaged, or destroyed.

Your business assets aren’t just expensive—they keep your business running. With commercial property insurance, you’ll be able to afford repairs for necessary equipment after an unexpected event like a fire or a break-in.

A commercial property insurance policy can cover your:

Business-owned building

Commercial property insurance protects a building owned by your business against fire, vandalism, and other types of damage.

Computers and electronics

If computers, tablets, smartphones, or other company-owned devices are destroyed or damaged, commercial property insurance will cover your financial losses. However, for data loss, you’ll need to add electronic data processing insurance to be fully protected.

Furniture and fixtures

The furniture and fixtures inside your owned or rented building are protected by commercial property insurance.

Supplies and equipment

If your business’s office equipment or supplies are damaged, destroyed, or stolen, commercial property insurance coverage can help repair or replace them.

Inventory

Commercial property insurance protects your inventory against theft, fire, and other causes of loss.

Outdoor fixtures

Your policy also covers fences, signs, lighting, and other fixtures and exterior items owned by your business.

How much does property insurance cost?

Commercial property insurance costs an average of $67 per month. It’s often affordable for small business owners, with 35% of our customers paying less than $50 per month for their policy.

The cost of commercial property insurance is based on several factors, including:

- Type of business

- Location

- Property value

- Safety measures, such as sprinkler systems

- Coverage limits and deductible

- Coverage options and exclusions

Who needs commercial property insurance?

Landlords often require proof of commercial property coverage, liability coverage, or another type of business renter’s insurance from their business tenants. Though landlords carry property insurance for their buildings, they won’t take responsibility for any expensive business property a tenant keeps on site.

Additionally, lenders often mandate business property insurance for the life of the mortgage.

Even when it’s not required, commercial property insurance is a crucial part of risk management for any business that owns a building, valuable equipment, or expensive inventory. It helps your business recover financially from incidents such as:

- Fire

- Lightning

- Wind and hail

- Water damage

- Theft

- Vandalism

Remember, homeowner’s insurance doesn’t usually cover lost or damaged business property, so home-based businesses should also consider commercial property insurance.

This policy is especially important for certain professions, such as:

Retailers, wholesalers, and manufacturers

Property insurance is crucial for any business that sells, distributes, or manufactures goods. For example, if a pipe bursts in a grocery store, a commercial property policy would cover the cost of replacing all of the food that had to be thrown away.

If you rent a commercial space, you can purchase a policy that covers only owned items in the space. You may also need to insure equipment that you lease, depending on your arrangement with the owner.

IT and technology

Tech companies rely on their computers and other expensive electronics on a daily basis.

If a thief breaks into your office and makes off with thousands of dollars’ worth of monitors, PCs, and laptops, a commercial property policy will cover the cost of replacing the stolen items.

Construction

Construction companies and contractors rely on several different types of specialized property insurance to cover their risks. They might need contractor’s tools and equipment coverage to protect power tools that travel to different job sites, or builder’s risk insurance to cover a structure in progress.

If a fire destroys your tools and equipment, or someone vandalizes a construction site, these policies will help you recover financially.

Real estate

Commercial landlords, property managers, and other real estate professionals likely need a policy that covers the actual building and all contents, including mechanical and electrical systems.

If you rent a space, you may want to ask your tenants to carry insurance to make sure their own items are protected as well. You should also consider purchasing lessor’s risk only (LRO) insurance to protect yourself from legal fees if an accident happens on your property, as well as a building insurance policy, which covers property damage to buildings, structures, and completed additions that you lease to commercial tenants.

Top professions that need property insurance

What does commercial property insurance not cover?

Commercial property insurance covers a commercial building and its contents. However, it doesn’t cover every risk or type of property. Here are a few situations where you may need additional coverage:

Goods in transit and mobile equipment

If your business needs coverage for items in transit or equipment that moves to different worksites, consider inland marine insurance or equipment floater insurance. These policies cover equipment, tools, and other possessions that move from place to place. It also includes items in a business’s temporary care, such as loaned artwork.

Damaged customer property

General liability insurance covers property belonging to your customers and clients. It helps cover legal costs if someone sues over a broken item or an accidental injury.

Business interruption

Business interruption insurance, also called business income insurance, covers financial losses when a covered property claim forces a business to close temporarily. It can pay for loss of income, employee wages, and other day-to-day expenses.

This policy sometimes includes extra expense coverage, which covers costs beyond your routine operating expenses. For example, you might need to move to a temporary location or hire additional employees after a fire or other disaster.

Employee theft

Employee dishonesty coverage reimburses your clients if an employee steals items or money from them. This coverage includes fidelity bonds, which protect your business and clients against dishonest employees.

Malfunctioning equipment

Equipment breakdown coverage pays to replace malfunctioning equipment after a mechanical or electrical failure. You can add this extra coverage as an endorsement on your commercial property insurance policy.

Destroyed payment records

If a burst pipe or other incident destroys customer records, your business could have trouble collecting outstanding customer payments. This isn’t considered a covered loss of commercial property insurance, unless your policy has an accounts receivable endorsement.

Find general liability insurance quotes

FAQs about property insurance

Get answers to frequently asked questions about commercial property insurance

How does commercial property insurance work?

Commercial property insurance usually covers damage caused by named perils. That includes burglaries, vandalism, fires, and windstorms. But it doesn’t cover normal wear and tear, natural disasters (such as a hurricane), and many other types of risks.

Typically, this policy covers your building and business personal property kept at that location. If you don’t own or rent a building or other commercial space, the policy can cover assets stored at a designated location. These are usually places like your home or a storage unit.

Commercial property insurance coverage offers policyholders a choice of receiving cash value or replacement value for stolen or destroyed items. An actual cash value policy costs less, but pays out only what the item is currently worth. Due to depreciation, you might have to pay money out of pocket toward the replacement cost.

Opting for replacement value means that the carrier will reimburse the lost equipment with a brand-new equivalent. While replacement value policies have a higher insurance rate, the extra cost may be beneficial for businesses that depend on state-of-the-art equipment, such as many IT companies.

What are the exclusions on commercial property insurance?

Commercial property insurance has some coverage exclusions. For example, it usually doesn’t pay for property damage caused by natural disasters like earthquakes, hurricanes, tornadoes, and floods. If you need coverage for these events, you can add an endorsement to your policy.

It also doesn’t cover damage caused by short circuits, power surges, or loss of pressure. An equipment breakdown endorsement extends coverage to damage caused by these events.

Additionally, it won’t cover business vehicles. If your business owns a company vehicle, you’ll typically need to purchase commercial auto insurance to comply with state law.

You can add endorsements (riders) to your policy to fill other gaps in coverage too. Check with an Insureon agent to make sure your insurance policy includes the type of coverage you need.

Is it possible to combine my property coverage with other policies?

Yes. Many companies that own or rent their workspace bundle their property coverage with general liability insurance in a business owner’s policy (BOP).

A business owner’s policy comes in handy if your landlord requires you to have renter’s insurance, or you need general liability coverage in order to secure a contract with a client. It typically costs less than if the policies were bought separately. Most low-risk small businesses are eligible for a BOP.

Similar to a BOP, a commercial package policy (CPP) also packages property and liability coverage. A CPP offers more flexible protection options and is generally purchased by high-risk small and medium-sized businesses.

There are several types of liability insurance products that help pay for different kinds of lawsuits. They include:

- General liability insurance for common customer, copyright, and defamation lawsuits

- Professional liability insurance, also called errors and omissions insurance (E&O), for disputes over the quality of your work

- Cyber insurance for protection against data breaches and cyberattacks

- Employment practices liability insurance (EPLI) for violations of employee rights

An insurance agent can help you find cost-saving insurance bundles that fit your business.

Where can I learn more about commercial property insurance?

If you want to learn more about this policy, you can find additional answers in our frequently asked questions about commercial property insurance.

You can also consult with an insurance agent about your insurance needs and get free small business insurance quotes from top U.S. insurance companies.

Commercial property insurance cost

The cost of commercial property insurance varies based on a number of factors about your business. Your property insurance (also called hazard insurance) premium is directly impacted by the size of your building, the value of your business equipment, and more.

What is the average cost of commercial property insurance?

Small businesses pay an average premium of $67 per month, or about $800 annually, for commercial property insurance. Almost two-thirds (62%) of customers spend $100 or less for coverage.

Our figures are sourced from the median cost of policies purchased by Insureon customers from leading insurance companies. The median offers a better estimate of what your business is likely to pay because it excludes outlier high and low premiums.

Typical commercial property insurance costs for Swift Insurance customers

While Swift’s small business customers pay an average of $67 monthly for commercial property insurance, 35% pay less than $50 and 27% pay between $50 and $100 per month.

The cost varies for small businesses depending on their risks and the coverage they choose.

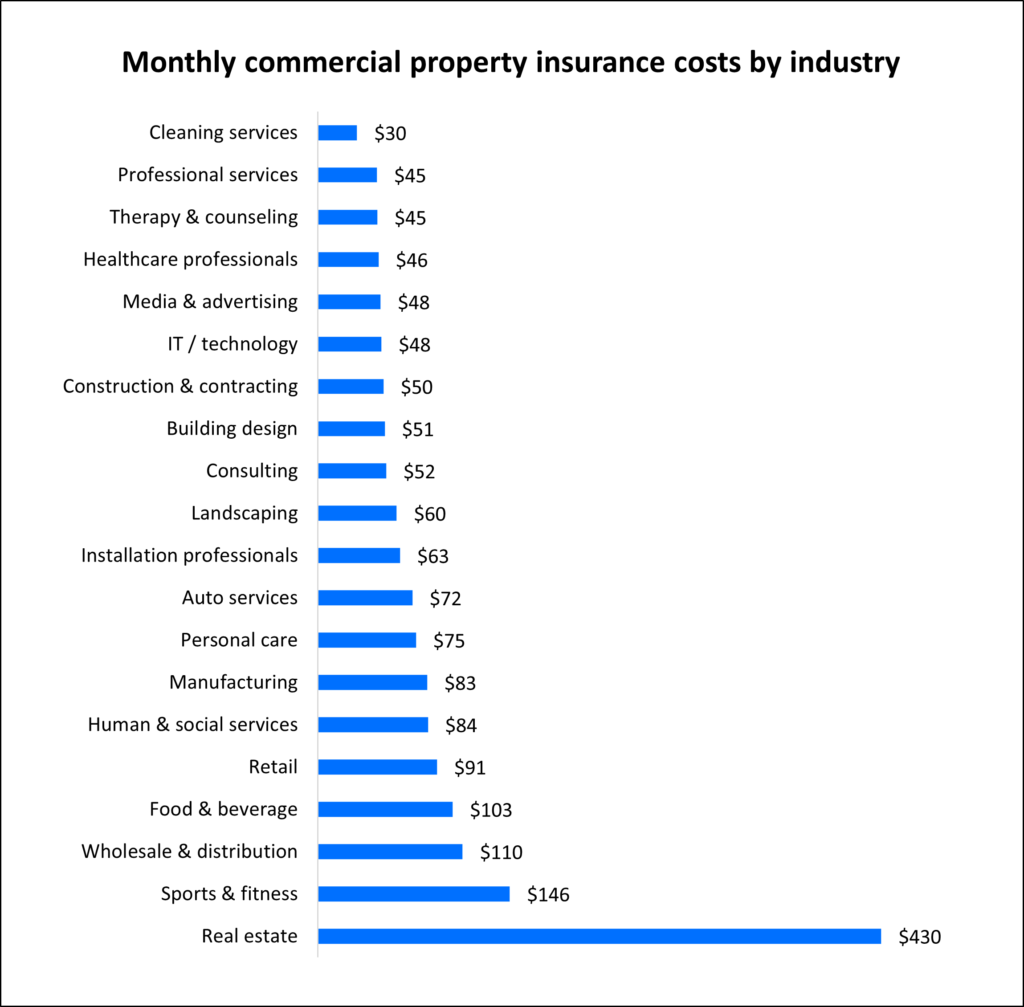

How does your industry impact the cost of commercial property insurance?

Our analysis of commercial property insurance costs reveals that for small businesses, your industry has one of the biggest impacts on your premium. Generally, insurance companies charge high-risk industries higher premiums, while low-risk industries enjoy lower rates.

For example, commercial landlords are exposed to more risk than IT consultants who work from a home office. The graph below illustrates how the type of business affects what you’ll pay for a commercial property insurance policy.

Depending on the industry that you work in, such as sports and fitness, you may be required by a property owner to carry commercial property insurance coverage in order to rent a space.

For other businesses, such as those in insurance or healthcare, you may need professional liability insurance (also called errors and omissions insurance) before you can get a license.

Understanding commercial property insurance cost factors

Insurance policies are not a one-size-fits-all product. Each company has different business needs based on a number of factors, and insurance companies will charge higher or lower rates depending on your company’s coverage needs and the type of policy you plan to purchase.

For commercial property insurance, these factors often include:

- Coverage limits and deductibles

- Size of business and number of employees

- Claims history

- Industry and risk factors

- Location

How do policy limits and deductibles affect commercial property coverage costs?

The policy limits and deductible you choose will impact the cost of your commercial property insurance. Generally, the higher your limit, the more expensive your premium will be.

Many policyholders bundle their commercial property coverage with general liability insurance in a bundle called business owner’s policy (BOP). A BOP is often less expensive than purchasing each policy separately.

High-risk small businesses and medium-sized businesses are advised to get a commercial package policy (CPP), which also bundles general liability insurance with commercial property but offers more coverage options than a BOP.

General liability insurance with $1 million / $2 million limits is the most popular option for small businesses. This includes:

- $1 million per-occurrence limit. While the policy is active, the insurer will pay up to $1 million to cover any single claim.

- $2 million aggregate limit. During the lifetime of the policy (usually one year), the insurer will pay up to $2 million to cover claims.

Almost all of Insureon customers (91%) choose a policy with $1 million / $2 million limits. Five percent of our customers choose a policy with $2 million / $4 million limits, the next most popular choice.

The deductible you select is another factor that will influence the cost of your commercial property coverage. You can save money on property insurance by choosing a higher deductible or lower limits. The average deductible that Insureon customers select for commercial property insurance is $1,000.

What other factors impact property insurance costs?

Your industry and policy limits are just a couple of factors mentioned that will impact your commercial property insurance rates.

Your insurance provider will also look at the following when calculating your premium:

1. Location

Your business location can help your provider determine which environmental risks your company may face, such as natural disasters like flooding, tornadoes, or hurricanes. Real estate value and local law can also affect what premiums you pay. Your monthly cost could go up if your property value is higher, for example.

2. Size of business premises

A large commercial building or factory will likely cost more to insure than a single rented room.

3. Safety and security

Is your business located in a high-crime area? Does your business possess toxic materials or engage in dangerous activities like mining? Do you have loose security measures that don’t protect your physical assets and encourage vandalism?

These are all higher risks and can affect your insurance rates. If you deal with toxic materials, it may be a good idea to obtain environmental insurance to provide liability coverage for pollution risks.

4. Fire protection

Property with easy access to a fire station and fire hydrants may cost less to insure. Sprinkler systems and fire alarms help reduce insurance costs, too.

Once you find the right policies for your small business, you can begin coverage in less than 24 hours and get a certificate of insurance for your small business.

5. Age of building

Old buildings can be more susceptible to certain types of property damage, so they may cost more to insure. For example, a fire caused by old electrical wiring could translate into costly repairs.

6. Age and type of equipment

Heavy industrial equipment will cost more to insure than an at-home business’s sewing machine.

You may also pay higher premiums if your equipment is hard to repair because of scarce parts, or if it’s more susceptible to equipment breakdown because of heavy use. Alternatively, it might be cheaper to repair older equipment than buy state-of-the-art technology.

If you have equipment that you bring from one job site to another, you may need inland marine insurance or contractor’s tools and equipment coverage. These policies protect your tools and other property while in transit.

7. Property valuation method

Replacement value coverage costs more than actual cash value coverage. The former payouts the replacement cost of a brand-new item, while the latter payouts the item’s depreciated value.

8. Types of hazards covered

Most commercial property insurance policies include hazard insurance in their coverage.

A policy that covers open perils costs more than a policy that covers named perils. Open perils coverage protects against all losses except those specifically excluded in the policy. Named perils coverage only protects against losses listed in the policy.

Top industries we insure

How can you save money on commercial property insurance?

It’s easy to save money on your commercial property policy without compromising on coverage.

Some strategies to keep costs down include:

- Bundle policies. To save money, many small business owners opt for a business owner’s policy (BOP) or commercial package policy (CPP), which combines commercial property insurance with general liability insurance at a lower rate than purchasing each policy separately.

- Pay the annual premium. When you purchase a commercial property policy, you can choose to pay your premium in monthly installments or annually. The annual amount is less expensive than paying by the month.

- Manage your risks. Claims on your insurance make your premium go up. You should try to reduce and/or prevent all types of risks to avoid claims and keep your premium down. This could look like investing in security systems and other preventative technologies to avoid claims.

- Choose a higher deductible. Selecting a more costly deductible is an easy way to save on your premium, but be sure to choose one that you can still afford. If you can’t pay your deducible, you can’t collect on a claim.

Why do small businesses choose Swift Insurance?

Swift is the #1 independent agency for online delivery of small business insurance. We help business owners compare quotes from top-rated providers, buy policies, and manage their different types of coverage online.

By completing Swift’s easy online application today, you can compare free quotes for business property insurance and other types of insurance from top-rated U.S. carriers.

Once you find the right policies for your small business, you can begin coverage in less than 24 hours and get a certificate of insurance for your small business.

Cheap commercial property insurance

You can save money on commercial property insurance by limiting your property damage risks and by comparing insurance quotes from different providers.

How do I find cheap business property insurance?

Commercial property insurance covers your business’s location and other assets like equipment and inventory. It pays to repair or replace these assets in case they’re stolen, lost, or damaged.

Your homeowner’s insurance won’t cover items that belong to your business, or it may provide limited coverage, which is why you may need this policy.

Starting at $29 per month, a commercial property insurance policy can be affordable for small businesses.

There are many ways for you to keep costs low. For example, you can compare rates from different insurance companies, such as through Swift’s easy online application that retrieves quotes from trusted carriers.

In addition, bundling your commercial property policy with other insurance products, choosing cost-saving options on your commercial property insurance coverage, and managing your risks to avoid insurance claims can also help you pay less.

1. Shop around and compare insurance quotes from multiple providers

Getting quotes from multiple insurance companies is one of the best ways to find affordable commercial property insurance. You could go straight to the source and contact each carrier directly, or you could work with an online insurance agency like Insureon for a simpler and easier experience.

At Swift, you can get commercial property insurance quotes from top-rated providers, such as The Hartford and Liberty Mutual, with a single online application. Our licensed insurance agents are available to help you customize a policy for your business’s unique needs, making sure you meet state laws and your profession’s requirements.

Once you select the commercial property insurance policy you need, you can get coverage and a certificate of insurance (COI) in less than 24 hours.

How much does commercial property insurance cost?

Swift’s small business customers pay an average of $67 per month, or about $800 per year, for business property insurance.

Key factors to determining the cost of commercial property insurance include:

- Your type of business

- Business location

- The size and type of property you have, including business assets

- Property value, including your equipment and inventory

- Safety measures, such as sprinkler systems

- Deductible, policy limits, and other coverage options

2. Bundle your business property insurance with other policies

One easy way to save money on your policy is to buy two types of insurance in a combined package. A business owner’s policy (BOP) combines commercial property coverage and general liability insurance in one policy. It’s usually less expensive than buying property and liability coverage separately.

A BOP typically provides coverage for:

- Injuries to customers, clients, and other third parties visiting your property

- Damage to property owned by your business or a third party

- Product liability insurance for items your business makes, sells, or distributes

- Libel, slander, and copyright infringement

3. Customize your commercial property insurance policy to reduce costs

While most property insurance policies offer similar coverage, you do have options for customizing your policy to keep insurance rates down.

Here are the most common cost-saving options:

Choose lower policy limits

The policy limit is the maximum amount your insurer will pay on a claim. For property insurance, your limits should match the value of your business’s property. That includes your building and your business personal property, such as inventory, office equipment, and furnishings.

Lower coverage limits cost less, but leave you open to financial risk. You’ll want to consider both the cost of insurance and how much you can expect to pay for a claim after a fire, storm, or other incident.

Choose a higher deductible

Your policy’s deductible is the amount you pay on a claim before your insurance coverage takes over. Higher deductibles are more affordable, but make sure it’s an amount you can afford in a crisis.

For example, a fire might damage your commercial building and computers. The cost of repairing the damage is estimated at $75,000 while your deductible is $1,000. You would pay the first $1,000. The insurance company would cover the remaining $74,000 in damages.

If your business losses are small enough that they fail to meet your deductible, you would have to cover any claims yourself. Some small business owners believe a higher deductible is worth it in the long run, as it reduces your premium while maintaining coverage in case of a significant loss.

Examine your policy’s exclusions

Every insurance policy comes with exclusions, which stipulate the kind of claims it won’t cover. For property insurance, common exclusions include risks like floods and earthquakes.

When you buy a policy, check to make sure it doesn’t have any exclusions for coverage that you might need. You can often purchase an endorsement for your policy, which provides additional coverage for certain risks.

An insurance agent can help you determine the risks your business needs to cover, and the ones you can safely exclude to save money.

Choose the option for actual cash value

There are two types of reimbursement for a business property claim:

- If you insure your business property for its replacement cost, your insurance company will cover the cost of replacing your lost or damaged property with entirely new items.

- Insuring for the actual cash value means your insurance will cover your physical assets for their depreciated value (the value of the used items) after a loss.

Replacement value coverage costs more, but pays out more on a claim. Insuring for actual cash value lowers your premium, but depreciation reduces the amount your provider would pay on a covered loss.

Pay the annual premium

Opting to pay your entire insurance premium once a year, rather than monthly, can earn you a discount from your insurance company. If you can afford it, it’s one of the easiest ways to save money on insurance.

Maintain continuous coverage

While it might be tempting to drop your property insurance coverage occasionally to save money, this can wind up being more expensive in the long run.

Insurance companies tend to increase premiums for those who frequently start and restart their coverage. You also leave yourself exposed to an expensive loss that your business would have to cover on its own, without insurance.

4. Manage your risks to avoid claims

The right approach to risk management can save you money on commercial property claims and help keep your premium low.

Install sprinkler systems and burglar alarms

Many insurance providers offer a discount on commercial property insurance if a business has a sprinkler system, smoke alarms, a central burglar alarm, and other safety features.

You may want to check with your insurance company before installing a system, to make sure you get one that qualifies. It’s also a good idea to check your local building codes to see if particular systems are required.

Inspect your property

Routine inspections of your property can help you spot potential problems and address them before they turn into an expensive claim. Make sure your burglar alarms and sprinkler systems are working properly, as well as your entrances and security doors.

It’s also a good idea to consider your surroundings and the exterior risks to your business. Examine features like tree limbs and power lines to make sure they don’t pose a threat in case of a windstorm or similar event.

Whatever risks you might face from wildfires, severe storms, floods, tornadoes, or hurricanes, could have increased over the past few years. Do what you can to protect your property from these risks and make sure you’re adequately insured.

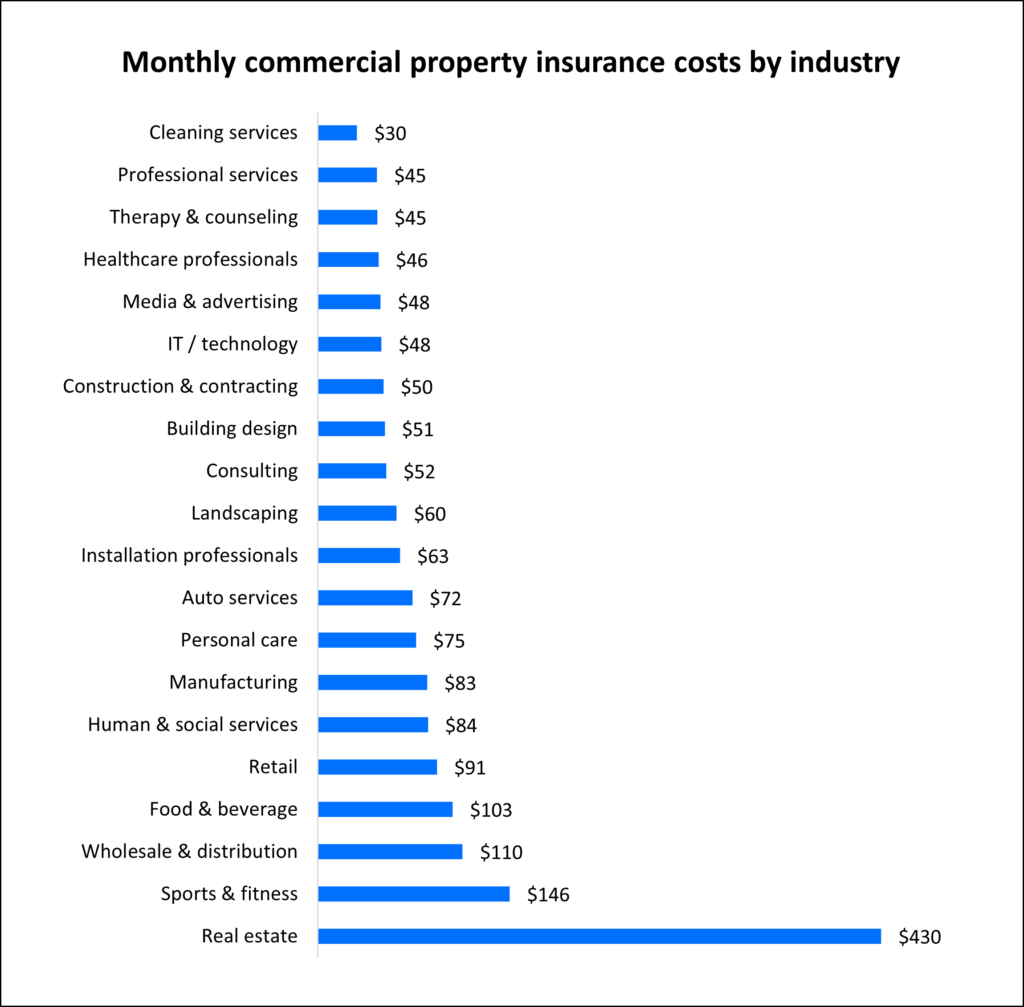

Cheapest industries to purchase commercial property insurance

In addition to your location, your industry can affect how much you pay for commercial property insurance.

Generally speaking, industries that tend to have business property that is lower in value and have less risk of property damage can expect to pay a smaller premium. For example, an IT consultant who works from a home office or a wellness counselor who has a home-based business would pay less than a retail business owner who has a storefront.

Among Insureon customers, industries such as cleaning, therapy and counseling, and those that offer professional services tend to pay less compared to more public-centered industries like real estate and sports and fitness.

Here’s a look at commercial property insurance costs for different professions.

What other types of business insurance do I need?

While commercial property insurance helps your business recover from fires and storms, you’ll likely need other types of insurance to fully protect your business.

You may also need the following small business insurance policies:

General liability insurance: This covers common business risks like customer injuries, damage to a customer’s property, and advertising injuries.

Business owner’s policy: A business owner’s policy bundles general liability insurance with commercial property insurance to protect against liability claims and property damage. It generally costs less than buying these two policies separately.

Commercial auto insurance: This policy covers vehicles owned by your business and is required in nearly every state. It typically pays for accidents, vehicle theft, weather damage, and vandalism.

Business interruption insurance: Also known as business income insurance, this policy supports your business during temporary closure due to catastrophic property damage, such as a fire or natural disaster. It helps payout loss of income, day-to-day expenses, and rent or relocation costs.

Workers’ compensation insurance: Workers’ comp is required in almost every state for businesses that have employees. It covers medical expenses for work injuries, which are not often covered by regular health insurance.

Equipment breakdown coverage: Pays to replace malfunctioning business equipment after a mechanical or electrical failure. You can add this extra coverage as an endorsement on your commercial property insurance policy.

Inland marine insurance: Protects business property in transit from one job site to another, or stored at an off-site location. This includes inventory, tools, and equipment.

Professional liability insurance: Also known as errors and omissions insurance (E&O), this policy covers the cost of client lawsuits over unsatisfactory work. Many states require that you hold professional liability coverage before you can submit your application for certain professional licenses.

Find affordable property insurance with Swift Insurance

Complete Swift’s easy online application today to get free quotes for commercial property insurance coverage from top-rated U.S. companies. You can also speak with an agent about the types of coverage your business needs and if there are any discount bundles available for commercial property and other types of business insurance.

Once you find the right policy, you can usually begin coverage and get your certificate of insurance in less than 24 hours.